Retirement Reimagined: Why 65 Is just a number

If you think retirement means getting a gold watch at 65, buying a caravan, and slowly fading into crossword puzzles and bowls, think again. That idea of retirement is younger than you might think, barely 150 years old.

Back in 1889, Otto von Bismarck came up with the world’s first state pension in Germany. The retirement age? Seventy. The catch? Hardly anyone lived that long. Retirement wasn’t about freedom, choices, or lifestyle design. It was simply society’s way of looking after those who could no longer work.

That world is gone. We’re living longer, healthier, and with more options than ever before. The question now isn’t if retirement is changing, but whether we can keep up with the pace of it.

The forces turning retirement upside down

A few mega-trends have made the old version of retirement look about as modern as a Nokia 3310.

- Longevity is booming. A 65-year-old couple today has a 50% chance one of them will reach 92. That’s not a 10-year retirement like our grandparents had, it’s more like three decades.

- Health spans are stretching. Sixty is the new forty. Many 70-year-olds now are fitter, sharper, and more active than 50-year-olds a generation ago.

- Work is unrecognisable. Careers are fluid, jobs change every 4–5 years, remote work is mainstream, and the gig economy means flexibility is king.

- Technology has levelled the playing field. You can run a business from Bali, consult from your couch, and Facetime the grandkids from literally anywhere.

These aren’t passing fads. They’re permanent shifts. Which means we need to ditch the old retirement blueprint and start sketching out something far more exciting.

What retirement might look like

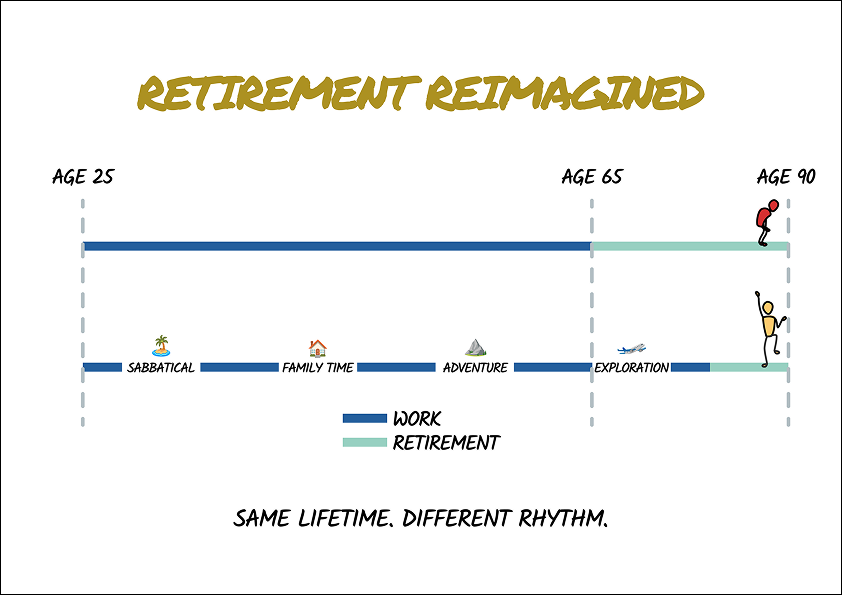

Forget the rigid “work until 65, stop forever” model. The future of retirement is flexible, experimental, and, dare we say it, fun.

- Career sabbaticals. Imagine taking 3–6 months off every few years to recharge, study, or finally tick off that bucket list item.

- Family-first breaks. Want to travel with your kids while they’re still little? Take a year off at 35 instead of waiting until 65. Those memories don’t come with a refund policy.

- Mid-life adventures. Why not test-drive your dream retirement at 45? Spend a year abroad and see if sipping wine in Tuscany every afternoon is all it’s cracked up to be.

- Shorter “traditional” retirement. With sabbaticals along the way, you might work longer overall but with far more energy, and by the time you reach 75, you’ve already lived much of your dream.

The big win? You’ll reach your later years with clarity, experience, and far fewer regrets.

Planning for multiple possibilities

Here’s the tricky bit: humans are rubbish at predicting what their future selves will want. The only way to know if you’ll actually enjoy a year of unstructured time is to try it.

That’s why the smart move is to build these experiments into your financial plan. Instead of saving for one big “retirement pot,” you could set aside funds for:

- Sabbaticals

- Location experiments

- Extended family adventures

The cost of these trial runs is usually much less than the value they add to your life.

The bottom line

The retirement of the future isn’t a single chapter, it’s a collection of seasons. Flexible, health-conscious, globally connected, and, if you plan it right, packed with adventure.

So don’t just plan for 65. Plan for 35, 45, 55, and beyond. Your financial future should be as dynamic as your life. And that’s exactly what we help our clients design.

*Main imiage from HUM